By Luke Smith · 2/2/2017

One of my favorite parts about leading datacenterHawk is having a front row seat to the changing data center market. I talk to colleagues in our industry frequently about the evolution taking place with data center users and providers, and the last few years have been fascinating. We’re on track for another active year in 2017, and below are five trends we believe will be present among North America data center operators.

They Will Expand in the Largest Markets

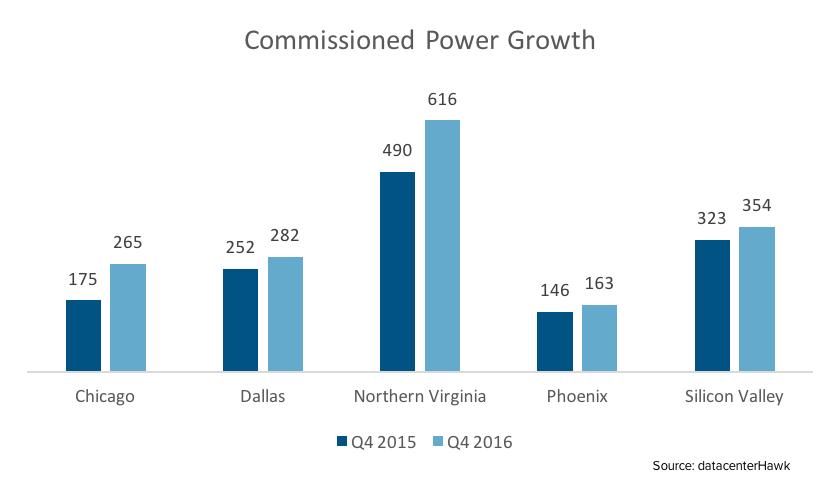

The largest data center markets grew the most in 2016, as areas like Chicago, Dallas, Silicon Valley, Northern Virginia, and Phoenix combined for nearly 300 MW of commissioned power growth (inclusive of pre-leasing). Smaller data center regions experienced little growth. The gap will likely continue to widen between these two types of data center markets, as larger cities have more capacity under construction and planned for the future.

Cloud Growth Will Continue in their Data Centers

Large cloud providers need capacity in major markets and their ability to grow quickly has increased in importance. As a result, cloud operators leased record capacity from data center providers in 2016. Lease transactions of this size have never been seen in the industry, some as large as 35 MW. An example of some of these transactions are listed below. Look for this trend to continue.

- 3Q 2016: CyrusOne – 13.5 MW in Phoenix

- 3Q 2016: RagingWire – 4.8 MW in Northern Virginia

- 3Q 2016: EdgeConneX – 18.0 MW in Chicago

- 3Q 2016: CyrusOne – 15.0 MW in Northern Virginia

- 3Q 2016: Vantage – 6.0 MW in Northern California

- 2Q 2016: CyrusOne – 18.0 MW in San Antonio

- 1Q 2016: DuPont Fabros – 16.0 MW in Northern California

- 1Q 2016: DuPont Fabros – 7.11 MW in Chicago

- 1Q 2016: CloudHQ – 35.0 MW in Northern Virginia

- 1Q 2016: Digital Realty – 5.4 MW in Chicago

- 4Q 2015: Digital Realty – 7.2 MW in Chicago

- 4Q 2015: CyrusOne – 22.5 MW in Northern Virginia

- 4Q 2015: CyrusOne – 9.0 MW in San Antonio

- 4Q 2015: DuPont Fabros – 10.4 MW in Northern Virginia

- 4Q 2015: DuPont Fabros – 6.0 MW in Chicago

M&A Market Activity Will Continue

Acquisitions significantly impacted the data center industry in 2016 and will continue in 2017. As competition increases and data center operators look to expand, acquiring other companies is the focus of several large operators. Vantage Data Centers is an M&A target for several companies in 2017, and it is likely Digital Bridge will be the buyer. 2016 examples of M&A activity include:

- Verizon’s data center portfolio was acquired by Equinix in December of 2016. The transaction will include 29 data centers in the United States and Latin America. Equinix will pay $3.6 billion for the business, and the transaction is expected to close in mid-2017.

- CenturyLink sold their data center business to Medina Capital and BC Partners in 4Q 2016. The $2.8 billion transaction will give Medina Capital nearly 2.6 million SF of data center space and will close within the first months of 2017. This was a long awaited announcement that should provide CenturyLink’s data center business future direction.

- DataBank was acquired by Digital Bridge. Included in the transaction were six data centers in Dallas, Minneapolis, and Kansas City. Although details on the transaction were not disclosed, DataBank was valued at several hundreds of millions of dollars. This acquisition provides DataBank expansion capital and expertise for future opportunities.

- TierPoint purchased CoSentry in 1Q 2016, adding nine Midwest data centers to their growing portfolio. After closing the deal in March, CoSentry became a subsidiary of TierPoint, and now operates under the TierPoint brand. These types of transactions are consistent with TierPoint, which has grown their data center portfolio primarily by acquisition.

Data Center Operators Will Grow with Campuses

Data center operators will continue to grow by acquiring large sites to build multiple facilities. The alternative of acquiring a smaller site holding only one facility can make expansion trickier. One of the catalysts to this growth method is large demand from cloud providers in major markets, and their need to grow quickly. By controlling the land for a campus build, data center operators are positioning themselves to handle these requirements.

Secondary Market Growth Still on Radar

Despite the activity occurring in major data center hubs, some operators will look to grow in secondary markets over the next year. Cities like Atlanta, Cleveland, Minneapolis, Nashville, Raleigh, Salt Lake City, and others will get significant looks from providers looking to take advantage of under-served cities. Opportunities exist with users who traditionally have owned and operated their own facilities or have placed their requirements in other cities because there is no credible data center operator in their current market. Examples of recent regional acquisitions include:

- H5 Data Centers recently purchased Cleveland Technology Center in Cleveland, OH

- DataBank announced this week the purchase of 365 Data Centers’ Cleveland, OH and Pittsburgh, PA facilities

- DataBank recently purchased C7 Data Centers in Salt Lake City, UT